To solve the problem of work-in-progress, we can calculate equivalent units of production (or “effective production”). The output of a department is always stated in terms of equivalent units of production. Since we are using FIFO method, we first include the entire beginning WIP in the cost of units transferred out and then include units started/added during the period. Thus, the 650,000 units that were completed are counted as 650,000 equivalent units of output no matter their physical origin from beginning inventory or otherwise.

Managerial Accounting

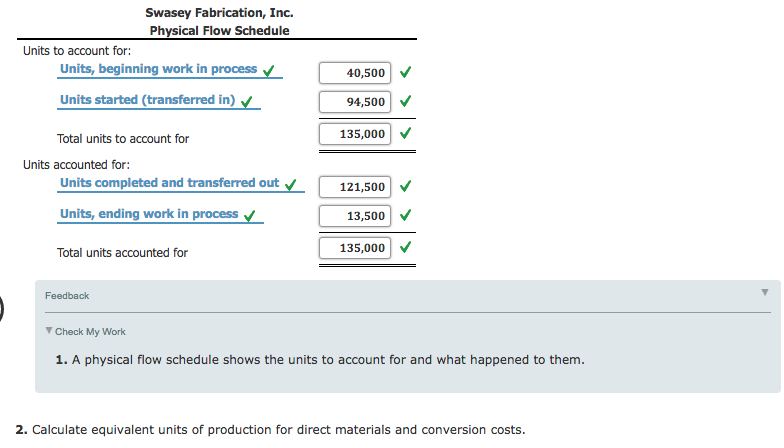

Although each department tracks the direct material it uses in its own department, all material is held in the material storeroom. Total costs to account for should always equal what was assigned in total costs accounted for. The table below summarizes the movement of physical units during the accounting period. Using the same example from the weighted average method, let’s use the following facts. In the next page, we will do a demonstration problem of the FIFO method for process costing. The units that remain in the ending work-in-process inventory, however, are not complete.

Equivalent Units – FIFO Method

A similar process is used to account for the costs completed and transferred. Reconciling the number of units and the costs is part of the process costing system. The reconciliation involves the total of beginning inventory and units started into production. Units completed and transferred arefinished units and will always be 100% complete for equivalent unitcalculations for direct materials, direct labor and overhead.

Physical Units

- Units started and completed are always 100% complete for materials, labor and overhead!

- Accountants have devised the concept of an equivalent unit, a physical unit expressed in terms of a finished unit.

- This means those $15,000 of conversion costs end up redistributed across all equivalent units worked on this period because they’re included in the conversion cost per equivalent unit rate we just calculated.

- It would be natural to assume it is about 50% complete (and thus equal to 0.5 equivalent units).

It just doesn’t make sense to track how many milliseconds each worker spends on each product unit among a sea of identical product units moving down an assembly line. Now you can determine the cost of the units transferred out and the cost of the units still in process in the shaping department. Once the equivalent units for materials and conversion are known, the cost per equivalent unit is computed in a similar manner as the units accounted for.

Specifically, direct material costs are rarely incurred at the same time as labor and overhead costs. First, product costs (meaning direct materials, direct labor, and overhead). Process costing firms usually find it inefficient to trace any costs to individual product units, including costs that are traditionally considered direct materials or direct labor.

5 FIFO Rates and Cost Allocation (STEP #2 and STEP #

One thing to keep in mind when using the weighted average method, we don’t need to compute the equivalent units for the ones transferred out. Those are considered 100% complete for the work done in that department, otherwise they wouldn’t be moving forward to the next process. Equivalent Units of Production is a more accurate method to determine whether the proposed output of the process will be able to meet or exceed that budgeted for. It allows us to accurately calculate if we are meeting our production.

We call the sum of labor and overhead conversion costs because they are costs incurred to convert raw materials into finished goods. This type of assessment must be repeated for direct labor and overhead. If overhead is applied based on labor, the process is simplified because the “percent complete” would an overview of the american opportunity tax credit be the same for labor and overhead. Below I complete the same cost allocation example as with the weighted average method, but now with FIFO. I again assume materials are added at the beginning of the process, so ending WIP units are 100% complete with respect to direct materials and transferred-in costs.

This is always the case when there are beginning WIP equivalent units. If there are no beginning WIP units, the two methods operate in exactly the same way. Again, the only difference between the two methods is that stinking beginning WIP. In short, these are common examples where 100% of direct materials are added at the beginning of the process. Thus it would be appropriate for process costing to reflect 100% of direct material cost being incurred at the beginning of the process. In Chapter 4, I made a parenthetical comment about dividing overhead evenly between individual product units.

Navarro started the month of June with 300,000 tons of iron ore in process in the Melting Department. During June, an additional 600,000 tons were introduced into the melting vats. In our next section, we will do a comparison and reconciliation of the same number of products through one process with each of the two methods. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

All of the materials have been added to the shaping department, but all of the conversion elements have not; the numbers of equivalent units for material costs and for conversion costs remaining in ending inventory are different. All of the units transferred to the next department must be 100% complete with regard to that department’s cost or they would not be transferred. So the number of units transferred is the same for material units and for conversion units. The process cost system must calculate the equivalent units of production for units completed (with respect to materials and conversion) and for ending work in process with respect to materials and conversion.